The National Labour Inspectorate (PIP) will be able to establish employment relationships without a court

Author:

Kirill Smirnov

Updated:

18/5/2026

Reading time:

nnn

min

Fundamental changes are taking place in Polish legislation that will directly affect every entrepreneur and foreign specialist. The law of March 11, 2026 (Act amending the Act on the National Labour Inspectorate) grants inspectors powers that previously belonged exclusively to courts.

For businesses and foreign professionals in Poland, this means the necessity to review current contracts. We explain how the new law will work and who it will affect first.

Deadlines and legal status of the reform

The new rules come into force on July 8, 2026. It is important to note that the law was sent to the Constitutional Tribunal for review, but this does not suspend its application. Starting in July, inspectors will begin working according to the new protocols.

The state has established a 12-month transition period. Companies that voluntarily bring their contracts into compliance with the actual nature of work within a year will be able to avoid liability for violations.

New procedure: from courts to administrative decisions

Before the adoption of the new amendments, a PIP inspector, upon discovering during an inspection that a person was working on an umowa zlecenie (civil law contract) but was actually performing the duties of a full-time employee, could only file a lawsuit in a labor court.

Court proceedings lasted for years.

Now the procedure becomes two-step and fast:

Order: Upon finding violations, the inspector issues a mandatory order to eliminate them.

Administrative decision: If the order is not fulfilled, PIP initiates proceedings and issues a decision on the existence of an employment contract.

Main change: the decision comes into force immediately regarding registration in the ZUS system and payment of taxes.

Now, it is not the inspector who goes to court to prove the employer's guilt, but the employer who is forced to go to court to challenge the already made PIP decision.

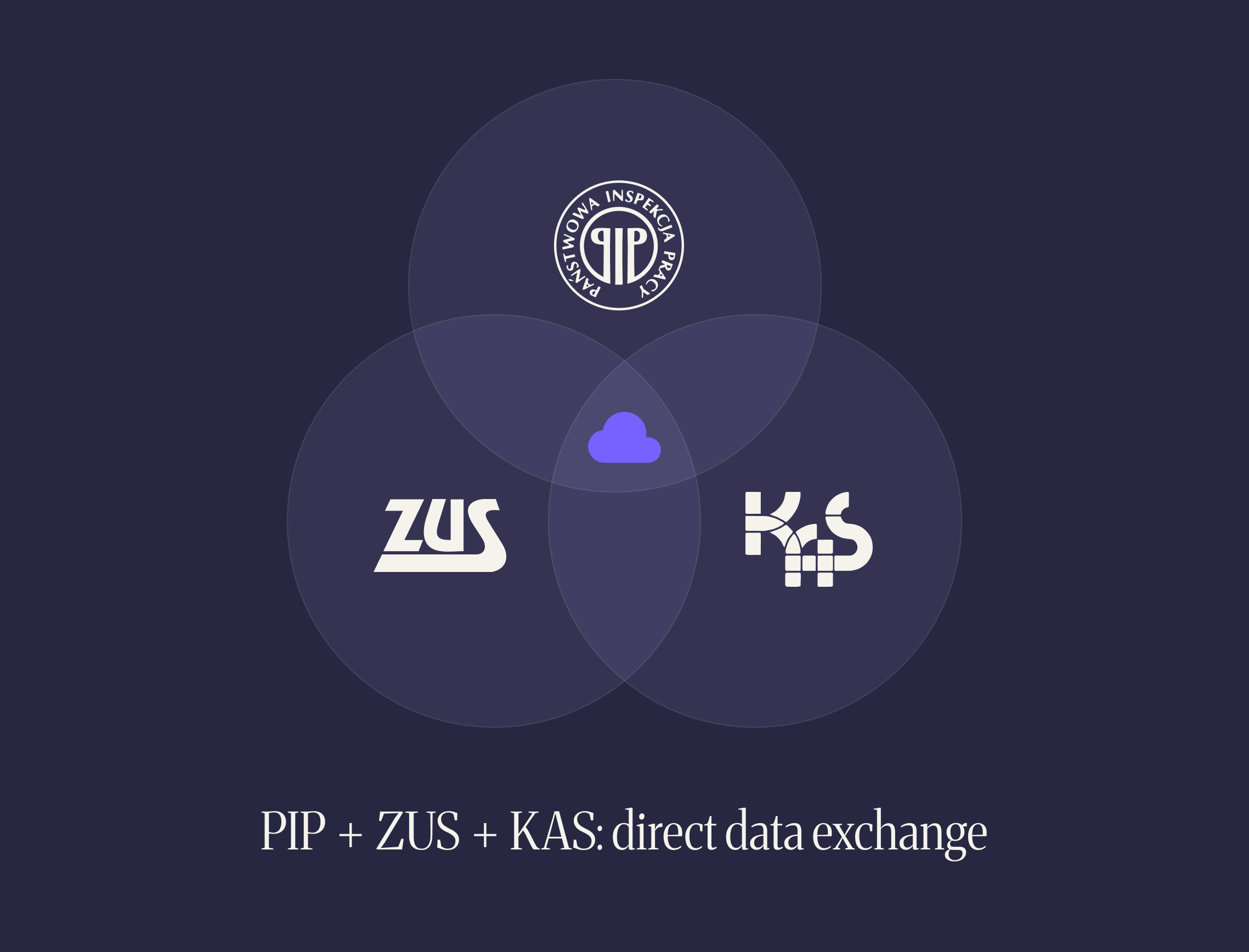

Digital supervision: automatic control through ZUS and KAS

The era of random "complaint-based" inspections is a thing of the past. The reform introduces a system of automatic data exchange between three state authorities:

PIP (National Labour Inspectorate);

ZUS (Social Insurance Institution);

KAS (National Revenue Administration).

This means a transition to a model of digital supervision. Algorithms will be able to automatically identify companies whose payouts on B2B contracts or umowy zlecenie suspiciously resemble the fixed salary of a full-time employee.

In addition, the possibility of remote inspections is introduced, which significantly increases the coverage of the inspectorate.

Signs of a "hidden" employment contract

The inspectorate will look not at the name of the document, but at the actual working conditions (according to Art. 22 of the Labor Code of the Republic of Poland).

Your contract is at risk if the following are present:

Hierarchical subordination: execution of direct orders from management.

Time and place control: the obligation to be in the office or online at strictly defined hours.

Personal performance: the inability to delegate tasks to a subcontractor (critical for B2B).

Company tools: using the employer's equipment and software without having your own economic risks.

New fines: liability has doubled

The reform significantly increases financial pressure on violators. Fines for key articles are almost doubled:

For replacing an employment contract and violating employee rights: from 2,000 to 60,000 PLN.

For repeated or gross violations: up to 90,000 PLN.

For an attempt to "take revenge" on the employee (for example, terminating the contract immediately after a PIP inspection): a fine of up to 60,000 PLN.

In addition to fines, the PIP decision automatically obliges the employer to additionally charge all ZUS contributions and taxes for the entire period of the recognized employment relationship.

How to protect your business?

The state effectively transfers part of the judicial functions to the administrative sphere, lowering the level of procedural guarantees for businesses.

In these conditions, the only way to avoid huge fines is a preventive audit.

ELPOFFICE specialists will help you:

Analyze current B2B contracts and Umowy Zlecenie for compliance with the new requirements.

Identify the risks of "hidden employment relationships" before they are detected by the PIP algorithm.

Develop a strategy for transitioning or adjusting cooperation conditions within the 12-month grace period.

Contact us for a consultation so that your business in Poland remains safe under the protection of professionals.

Need help with taxes or JDG?

The ELP Office team will help you understand the nuances of Polish legislation.

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu fugiat nulla pariatur.

Wakacje składkowe allows an entrepreneur to receive an exemption from paying their own social contributions for one selected month of the year.

During that month, the entrepreneur:

continues operating the business;

may earn income;

issues invoices as usual;

remains registered with ZUS;

maintains social insurance coverage.

The exempted contributions are paid from the state budget. Therefore, the month covered by wakacje składkowe is taken into account when future pension and social insurance rights are calculated.

Applications have been accepted since 1 November 2024. The first exemption was available for December 2024. As of July 2026, the main eligibility rules remain largely unchanged. Most updates have concerned the technical structure of the RWS form and the information required for de minimis aid.

Wakacje składkowe should not be confused with zawieszenie działalności. When using the relief, the business continues to operate. When business activity is suspended, the entrepreneur temporarily stops normal commercial activity.

Eligibility conditions

Who can use wakacje składkowe?

The relief is primarily intended for entrepreneurs operating a jednoosobowa działalność gospodarcza and registered in CEIDG.

A partner in a spółka cywilna may also use the relief, but the application concerns the partner’s personal contributions and must be submitted through their individual payer account.

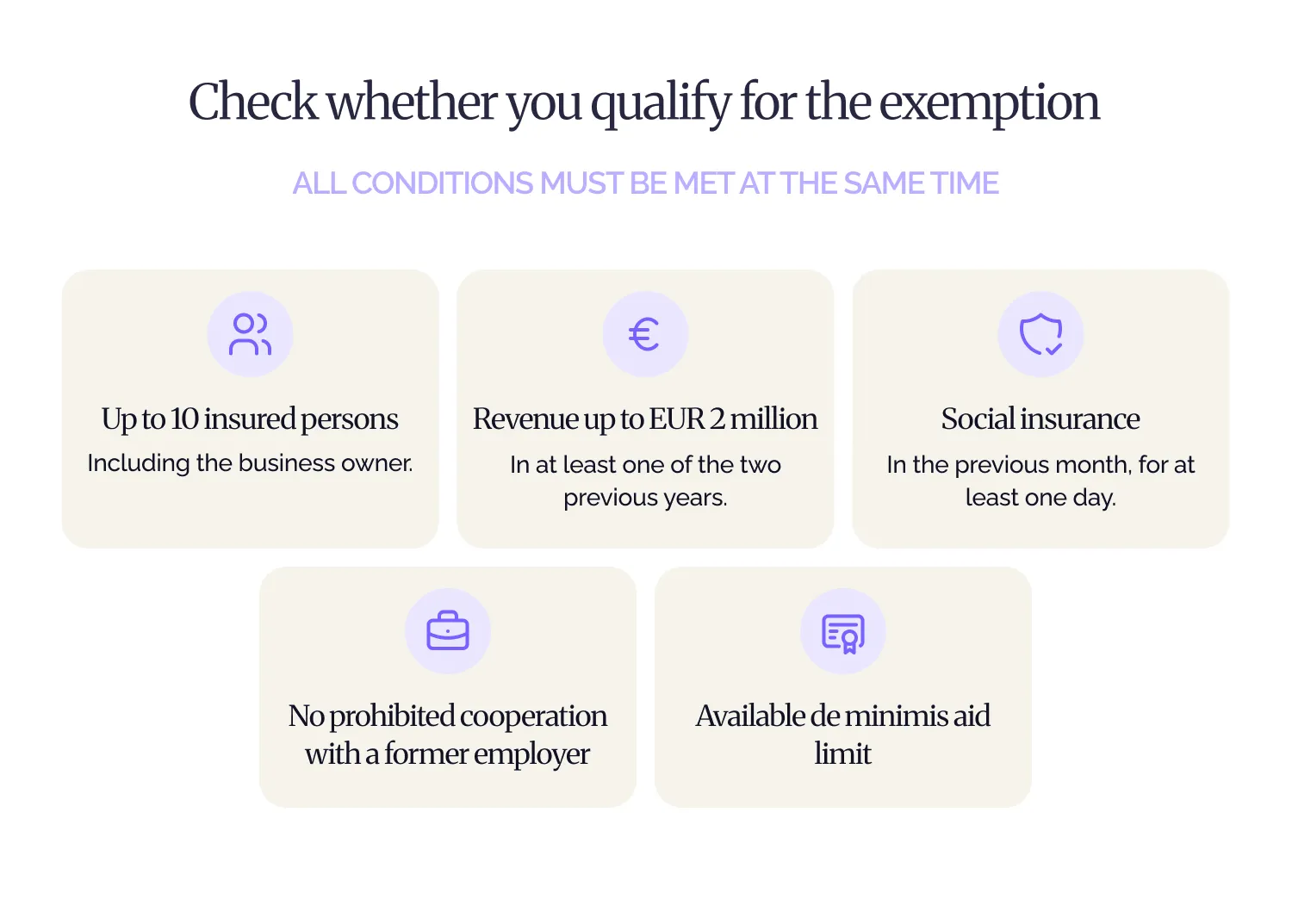

Several conditions must be met at the same time.

1. No more than 10 insured persons

In the month preceding the month in which the application is submitted, the entrepreneur must have no more than 10 insured persons registered with ZUS.

The entrepreneur is included in this limit. In a standard situation, this means the entrepreneur and no more than nine other insured persons.

The calculation may include:

employees;

zleceniobiorcy;

osoby współpracujące;

the entrepreneur.

A person registered for at least one day during the relevant month may be included. The calculation is not based only on the situation on the final day of the month.

For example, a person working under a short-term umowa zlecenie may still count toward the limit.

Students and pupils under the age of 26 working under an umowa zlecenie who are not subject to ZUS insurance are not included. Other exceptions may also apply, so borderline cases should be checked individually.

2. Revenue limit

The entrepreneur must meet the annual revenue requirement.

The relief is available if, in at least one of the two calendar years preceding the year of the application:

annual revenue did not exceed the equivalent of EUR 2 million; or

the entrepreneur did not receive any business revenue.

For an application submitted in 2026, the relevant years are 2024 and 2025. It is sufficient to meet the condition in one of those years.

3. No prohibited work for a former employer

The relief may be unavailable if the entrepreneur provides services to a former employer and performs the same duties that were previously performed under an employment contract in the year the business activity began or in the preceding year.

The cooperation is assessed for:

the calendar year preceding the RWS application;

the current calendar year up to the date of application.

The actual nature of the work is important, not only the title of the position or the wording of the contract.

Therefore, when moving from an umowa o pracę to B2B cooperation with the same employer, the previous duties should be carefully compared with the current scope of services.

4. Social insurance in the preceding month

The entrepreneur must have been subject to pension, disability and accident insurance for at least one day in the month preceding the RWS application.

There is no separate minimum period for operating a JDG. However, a newly established business may not always be able to use the relief immediately.

For example, if the JDG was registered on 1 May, the entrepreneur was subject to social insurance in May and submitted the RWS application in June, July may be selected as the exemption month, provided that all other requirements are met.

5. Available de minimis aid limit

Wakacje składkowe constitutes de minimis state aid. Before submitting the application, the entrepreneur should verify that the available de minimis aid limit has not been exhausted.

Who cannot use the relief?

The exemption will not be granted if the entrepreneur:

exceeds the insured-person limit;

does not meet the revenue requirement;

performs prohibited work for a former employer;

was not subject to social insurance in the preceding month;

has exhausted the de minimis aid limit;

has already used wakacje składkowe in the current calendar year;

submits the application outside the permitted period.

The relief is not available during ulga na start because the entrepreneur is not subject to the required social insurance during that period.

It may become available after moving to preferencyjne składki or another contribution scheme, provided that the remaining requirements are met.

Which contributions are covered and how much can you save?

Which contributions are covered?

The exemption applies only to the entrepreneur’s own social contributions.

It may cover pension, disability and accident insurance contributions, as well as voluntary sickness insurance and contributions to Fundusz Pracy and Fundusz Solidarnościowy where applicable.

Voluntary sickness insurance is covered only if the entrepreneur was subject to this insurance for at least one day both in the month of submitting the RWS application and in the preceding month.

The most important limitation is that składka zdrowotna is not covered by wakacje składkowe. It must still be calculated and paid under the standard rules.

Contributions for employees and other insured persons, taxes and previous ZUS arrears also remain payable.

How much can you save in 2026?

The amount saved depends on the entrepreneur’s social contribution scheme.

Based on the 2026 rates, the estimated exemption amount is shown in the table below.

Contribution scheme

Potential monthly savings

Standard minimum ZUS contributions including FP/FS

Up to 1,926.76 zł

Preferencyjne składki

Up to 456.18 zł

Mały ZUS Plus

From 456.18 to 1,788.29 zł

Składka zdrowotna must be paid separately.

The minimum monthly health contribution for the period from February 2026 to January 2027 is PLN 432.54 where the applicable taxation method and calculation base do not result in a higher amount.

The actual saving will therefore differ between entrepreneurs. It depends on:

the social contribution base;

whether voluntary sickness insurance is paid;

whether Fundusz Pracy and Fundusz Solidarnościowy apply;

the entrepreneur’s ZUS contribution scheme.

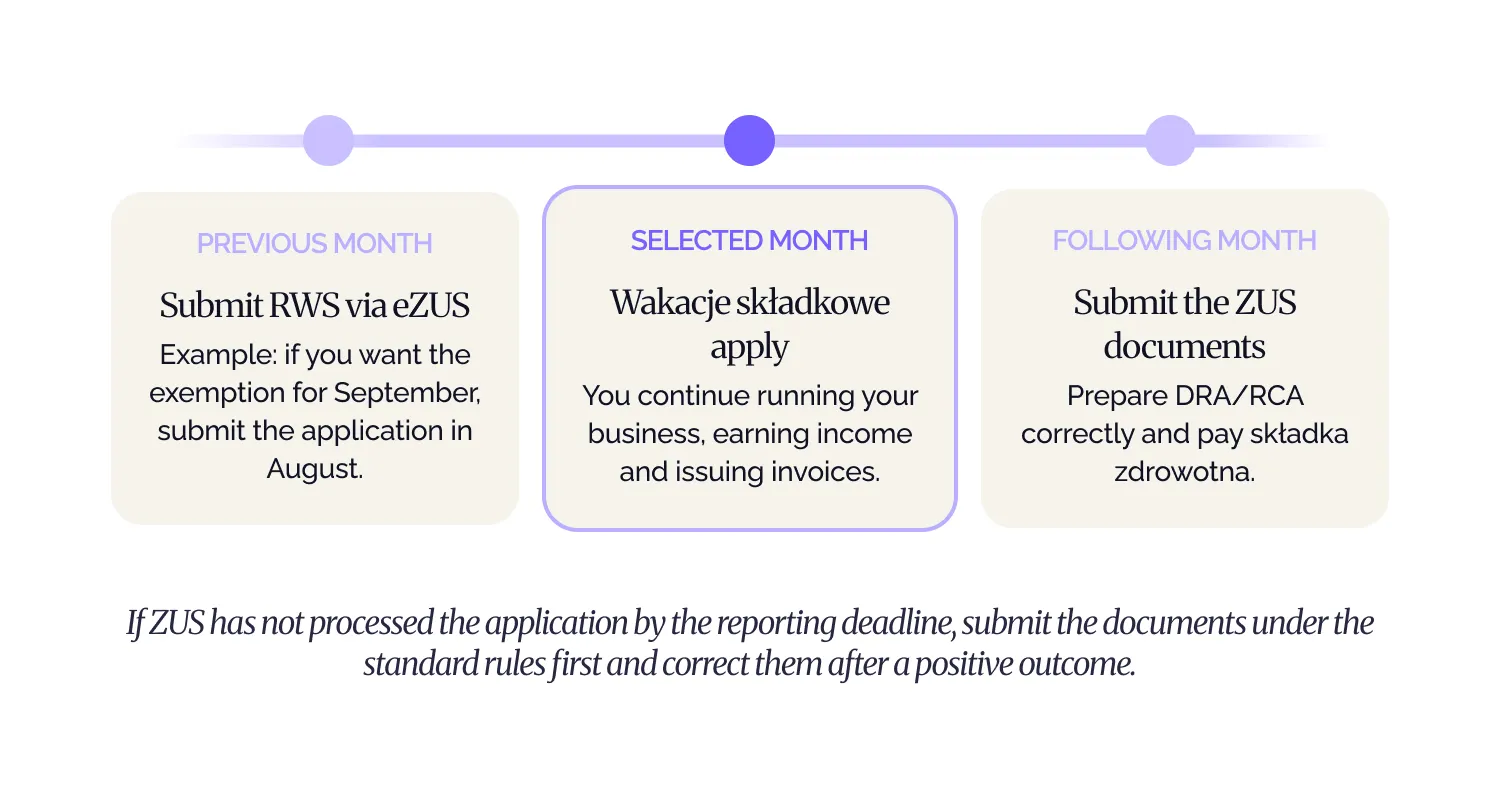

When and how to submit an RWS application

Which month can be selected?

The entrepreneur may select one exemption month in each calendar year.

The RWS application must be submitted in the month immediately preceding the selected exemption month.

For example:

Desired exemption month

When to submit RWS

August

In July

September

In August

October

In September

December

In November

The application cannot be submitted retroactively or several months in advance.

For example, to receive the exemption for August, the entrepreneur must submit the application in July. An application submitted in August may only concern September.

This is one of the most important rules. ZUS may leave an application without consideration if it is submitted outside the permitted month.

How to submit an RWS application through eZUS

The application must be submitted electronically through the konto płatnika in eZUS.

Before starting, prepare information about any de minimis aid received during the previous three years and check your main PKD code. Official certificates will only be required if you choose to confirm the aid through zaświadczenia.

Step 1. Log in to eZUS

Log in to eZUS and go to Konto płatnika.

The application must be submitted from the payer profile.

A wspólnik spółki cywilnej submits RWS through their individual konto płatnika, not through the company’s profile.

Step 2. Find the RWS form

In the side menu, select Katalog usług.

Then find:

Złóż wniosek o zwolnienie z obowiązku opłacenia składek za wskazany miesiąc (RWS)

Select Przejdź do usługi to open the application.

Step 3. Select the purpose and verify the details

For the first application, select Wniosek.

The entrepreneur’s details will be loaded automatically. Check them and complete any required fields that are missing.

Until ZUS reviews the application, it may be corrected or withdrawn using:

Uzupełnienie/korekta wniosku;

Wycofanie wniosku.

Step 4. Check the exemption month

In the Treść wniosku section, the system automatically displays the month following the month in which the application is submitted.

For example, if the RWS form is completed in August, it will concern September.

The month cannot be changed manually.

Step 5. Complete the Oświadczenia section

On this screen, two matters must be confirmed.

First, confirm that the revenue requirement is met: in at least one of the two preceding calendar years, revenue did not exceed the equivalent of EUR 2 million, or no business revenue was received.

Second, indicate whether de minimis aid was received during the previous three years.

If no aid was received, select:

Nie korzystałem z pomocy publicznej de minimis

If aid was received, select:

Korzystałem z pomocy publicznej de minimis

Then select how the aid will be confirmed:

Oświadczenie — complete the information about the entities from which de minimis aid was received;

Zaświadczenia — attach the official certificates at the end of the application.

Step 6. Complete the business information

Select the actual size of the enterprise. For many small JDG businesses, the appropriate option will be mikroprzedsiębiorstwo.

Next, choose the classification version in the Wersja PKD field:

PKD 2007;

PKD 2025.

Then select the main activity code corresponding to the information registered in CEIDG.

Until 31 December 2026, the application allows PKD 2007 or PKD 2025. After that date, PKD 2025 will be required.

The form will also ask additional questions concerning:

links with other enterprises;

mergers, divisions or business transformations;

activity in agriculture, fisheries or aquaculture.

For a standard JDG that is not linked to other companies, has not undergone a reorganisation and does not operate in these sectors, the usual answer is NIE.

If TAK is selected, the form will request additional information.

Step 7. Add attachments

If Zaświadczenia was selected in the de minimis section, attach the official certificates confirming the aid received.

If Oświadczenie was selected, the relevant information is completed directly in the application and separate certificates are not required.

Step 8. Check the application

At the Podsumowanie stage, open Widok danych dokumentów.

Check:

the entrepreneur’s details;

the exemption month;

information about de minimis aid;

enterprise size;

PKD version and code;

attachments.

If an error is found, return to the previous section and correct it.

Step 9. Sign and submit RWS

Select Podpisz i wyślij, choose one of the available signature methods and submit the application.

After submission, the application status and new ZUS messages can be checked in Sprawy płatnika.

A notification about a new document may also be sent to the email address or telephone number registered in eZUS.

Can the application be corrected or withdrawn?

Until ZUS reviews the application, it may be supplemented, corrected or withdrawn through the RWS form.

The selected exemption month cannot be changed. In that situation, the application must be withdrawn and a new one submitted within the permitted period.

Once the application has been reviewed, it can no longer be corrected or withdrawn through this procedure.

What happens after submission?

If ZUS grants the exemption in full, a separate administrative decision may not be issued. Information about the relief will appear in eZUS.

ZUS will issue an administrative decision if it:

refuses the exemption;

grants it only partially;

later determines that the eligibility conditions were not met.

Receiving the relief does not remove ZUS reporting obligations

Wakacje składkowe exempts the entrepreneur from their own social contributions for the selected month, but it does not remove the obligation to submit settlement documents.

For the exemption month, the entrepreneur must correctly prepare ZUS DRA and, where required, ZUS RCA.

Składka zdrowotna remains payable.

If ZUS has not reviewed the RWS application by the reporting deadline, the entrepreneur should not omit the declaration. The documents should first be submitted under the standard rules and then corrected after the exemption is granted.

It is advisable to inform the accountant in advance about the month selected for wakacje składkowe. This makes it easier to submit the application on time and settle the reporting period correctly.

Insurance, taxes and other reliefs

Does the insurance record remain continuous?

Wakacje składkowe does not create a break in social insurance.

The contributions for the exemption month are financed by the state and are taken into account when future pension and disability benefits are calculated.

Continuity of social insurance rights is also maintained, provided that the general eligibility requirements for the relevant benefits are met.

This is different from ulga na start, during which social contributions are not paid and the corresponding social insurance rights do not arise.

How does the relief affect taxes?

The social contributions, Fundusz Pracy and Fundusz Solidarnościowy amounts covered by the exemption are not subject to PIT.

At the same time, they cannot be treated as a tax-deductible expense because the entrepreneur did not pay them from their own funds.

Składka zdrowotna is calculated and treated under the standard rules applicable to the entrepreneur’s chosen taxation method.

Wakacje składkowe and other reliefs

Scheme

Main principle

Can you continue operating?

Key limitation

Wakacje składkowe

Exemption from the entrepreneur’s own social insurance

contributions for one month

Yes

The application must be submitted in advance, while the health

insurance contribution remains payable

Ulga na start

No social insurance contributions are payable at the beginning

of the business activity

Yes

There is no social insurance coverage or entitlement to

the related benefits

Preferencyjne składki

A reduced social insurance contribution base applies

for 24 months

Yes

The amount saved through wakacje składkowe will be lower

Mały ZUS Plus

The social insurance contribution base depends on income

Yes

Separate eligibility limits and deadlines must be observed

Zawieszenie działalności

Temporary suspension of business activity

Regular ongoing business activity is restricted

This is not a contribution relief scheme for an actively

operating business

Wakacje składkowe may be combined with:

preferencyjne składki;

Mały ZUS Plus.

The entrepreneur must still meet the general wakacje składkowe requirements.

The relief is not available during ulga na start because the entrepreneur is not subject to the required social insurance during that period.

Common mistakes

Submitting the application in the wrong month

RWS may only be submitted in the month directly preceding the exemption month. It cannot be submitted retroactively or two months in advance.

Incorrectly counting insured persons

Entrepreneurs sometimes count only permanent employees or check the situation only on the last day of the month.

However, a person insured for even one day may be included in the limit.

Assuming that nothing is payable

Składka zdrowotna, employee contributions and taxes remain payable.

Failing to verify de minimis aid

Incomplete or incorrect information may result in a request for additional documents, refusal of the relief or its later cancellation.

Waiting for the result and failing to submit DRA/RCA

If ZUS has not reviewed the application by the reporting deadline, the documents must be submitted under the standard rules and corrected later.

Failing to verify chorobowe coverage

Dobrowolne ubezpieczenie chorobowe is covered only if the entrepreneur was subject to it for at least one day in both the month of application and the preceding month.

Failing to analyse work for a former employer

ZUS assesses the duties actually performed, not only the wording of the contract.

If ZUS later determines that the requirements were not met, the exemption may be cancelled. The entrepreneur may then have to pay the contributions together with interest.

Frequently asked questions

Is it necessary to suspend the JDG?

No. During wakacje składkowe, the entrepreneur may continue working, earning income and issuing invoices.

Is składka zdrowotna still payable?

Yes. The exemption does not cover the health contribution.

Are employee contributions covered?

No. The relief only applies to the entrepreneur’s own contributions.

Is the relief available with preferencyjny ZUS?

Yes, provided that the general conditions are met. The saving will be lower because the social contributions are already reduced.

Is the relief available with Mały ZUS Plus?

Yes, if the entrepreneur meets both the wakacje składkowe requirements and the requirements of Mały ZUS Plus.

Can wakacje składkowe be used during ulga na start?

No. During ulga na start, the entrepreneur is not subject to the social insurance required for wakacje składkowe.

Can the application be submitted retroactively?

No. RWS must be submitted in the month preceding the selected exemption month.

Is a new application required every year?

Yes. A separate RWS application must be submitted for the selected month in each calendar year.

Can RWS be withdrawn?

Yes, but only until ZUS reviews the application.

Will there be a break in the insurance record?

No. The exempted contributions are financed by the state, so continuity of social insurance is maintained.

Summary

Wakacje składkowe allows an entrepreneur to reduce the cost of their own social contributions once per year without suspending business activity.

However, it is not an automatic “month without ZUS”. To use the relief, the entrepreneur must:

verify the eligibility requirements;

select the exemption month;

submit RWS in the preceding month;

provide the required de minimis information;

continue paying składka zdrowotna;

correctly prepare DRA and RCA.

Particular attention should be paid to the application deadline, the insured-person limit and cooperation with a former employer. An error in any of these areas may result in refusal or later cancellation of the relief.

Planning to use wakacje składkowe? ELP Office specialists can help verify the conditions, prepare the RWS application and correctly reflect the exemption in ZUS settlements.

e-Doręczenia is the electronic equivalent of a registered letter with proof of delivery. The system can be used to submit applications, receive decisions from public authorities, and retain official proof that documents have been sent and delivered.

An e-Doręczenia address cannot be replaced with a standard company email address. It is a unique technical address registered in the official Electronic Address Database — Baza Adresów Elektronicznych, or BAE.

It may look like this:

AE:PL-12345-67890-ABCDE-12

The address makes it possible to identify the sender and recipient and confirm the date and time when correspondence was transmitted.

Personal and business correspondence use separate addresses. Therefore, even if someone already has a personal e-Doręczenia inbox, they must create a separate business address for their activity registered in CEIDG.

ePUAP has not disappeared completely. However, since 1 January 2026, e-Doręczenia has been the main channel for official electronic correspondence. Other communication methods may still be used where special regulations or a specific electronic service allow them.

Who must have an e-Doręczenia address?

The registration deadline depends on the register in which the business is entered and the date of registration.

Category

When the obligation arises

Companies and sole proprietorships registered in KRS or CEIDG

from January 1, 2025

Upon business registration

Companies registered in KRS before January 1, 2025

From April 1, 2025

Sole proprietorships registered in CEIDG before January 1, 2025

From October 1, 2026

Sole proprietorships in CEIDG that change their registry data

after June 30, 2025

Upon submitting a data change application

Advocates, notaries, tax advisors, and other public trust

professionals

From January 1, 2025

Sole traders registered in CEIDG before the end of 2024 must therefore activate their address no later than 30 September 2026.

However, it is not always possible to wait until that date. If an entrepreneur changes their CEIDG details after 30 June 2025, the information required to create an e-Doręczenia address becomes a mandatory part of the application.

This may apply, for example, when:

changing the business address;

suspending or resuming business activity;

changing PKD activity codes;

adding or changing an authorised representative;

making other updates to the CEIDG entry.

Why the inbox must be checked regularly

The e-Doręczenia system applies the principle of deemed delivery — fikcja doręczenia.

If correspondence from a public authority is delivered to the inbox of a company or entrepreneur but is not received earlier, it is considered legally delivered on the day following the end of the 14-day period calculated from the date of receipt indicated in the delivery confirmation.

That date is treated as the official date of service. Deadlines for responding, submitting documents, or filing an appeal are calculated according to the rules applicable to the relevant procedure.

As a rule, the absence of an email notification, the owner’s holiday, or irregular inbox checks do not suspend statutory deadlines.

What may happen if the inbox is not created or checked

The e-Doręczenia Act does not impose a separate automatic fine solely for failing to have an address. The main risk is missing legally significant correspondence and the deadlines connected with it.

If the recipient does not have an active e-Doręczenia address, a public authority may, where permitted by law, use the Public Hybrid Service — Publiczna Usługa Hybrydowa, or PUH.

The document is transferred electronically to the operator, printed, and delivered to the recipient in paper form.

Once the address has been activated, it is particularly important to monitor incoming messages regularly. Missing a deadline may mean that the entrepreneur does not have enough time to submit documents, respond to a request, or appeal a decision.

In tax proceedings, an authority may impose a kara porządkowa, or procedural fine, in the circumstances listed in Article 262 of the Polish Tax Ordinance. In 2026, the maximum amount is PLN 3,800.

This is not a fine for simply having or not having an e-Doręczenia inbox. It may be imposed for a specific procedural violation, such as failing to comply with a properly delivered request where tax law allows such a penalty.

How to create an e-Doręczenia address for a sole trader

For a sole trader registered in CEIDG, creating an e-Doręczenia address usually takes little time. Most information is retrieved automatically, and the application can be signed using Profil Zaufany.

The process is similar to creating a personal e-Doręczenia inbox. However, the applicant must select registration of an address specifically for business activity.

Important: a personal e-Doręczenia address and a sole trader’s business address are two separate addresses. Official correspondence relating to an activity registered in CEIDG requires a separate business address.

What to prepare before you start

You will need:

Profil Zaufany, e-dowód, or a qualified electronic signature;

the administrator’s details if another person will manage the inbox.

A sole trader may manage the inbox personally. An accountant or another user can be added later, after the address has been activated.

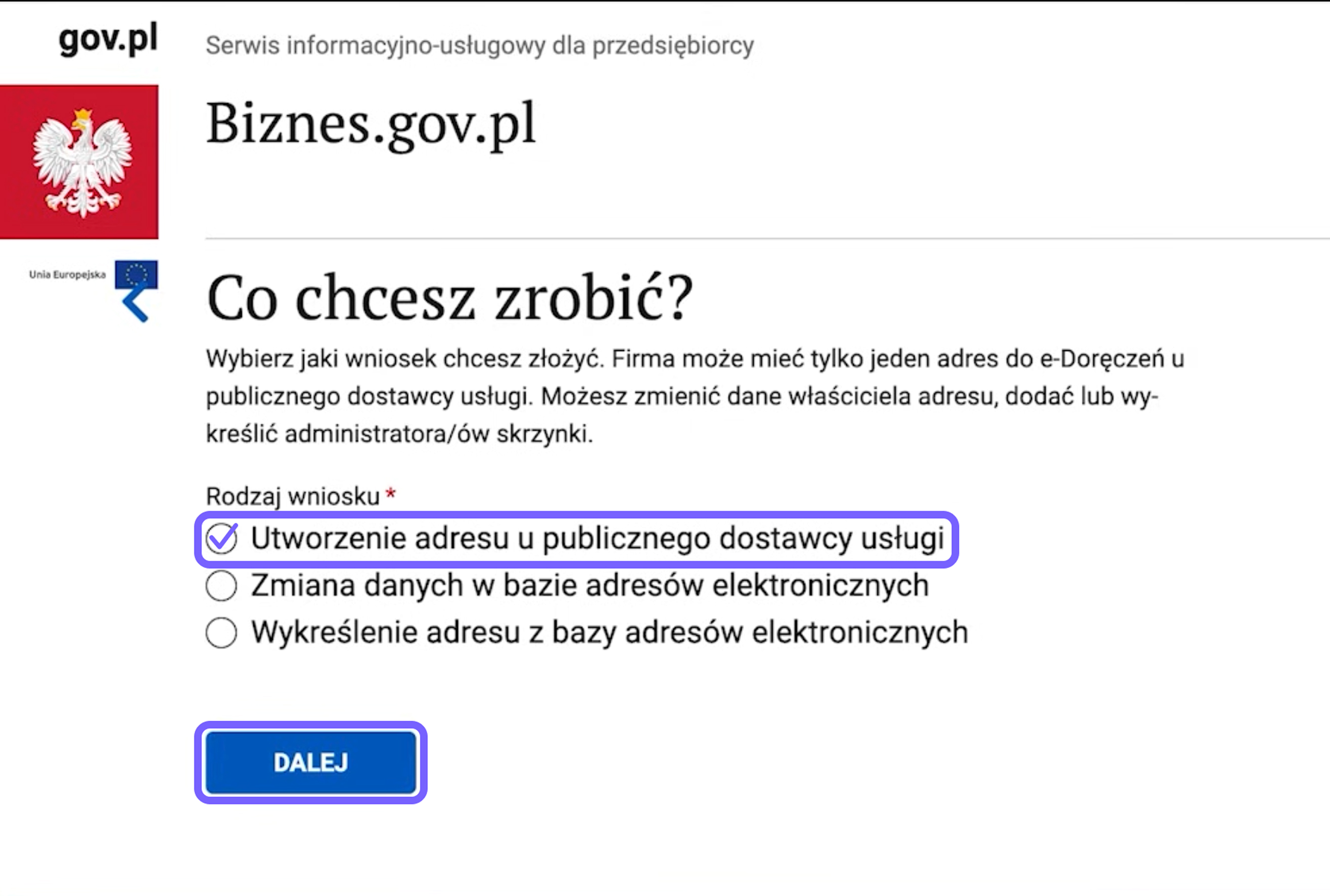

Step 1. Open the address creation service

Log in to Konto Przedsiębiorcy on Biznes.gov.pl and open the service for creating an e-Doręczenia address.

On the start screen, click:

Złóż wniosek — Submit an application.

Step 2. Select the public service provider

The system will ask how you want to create the address. Select:

Utworzenie adresu u publicznego dostawcy usługi — Create an address with the public service provider.

This is the free option intended for official correspondence with public authorities.

Click Dalej — Next.

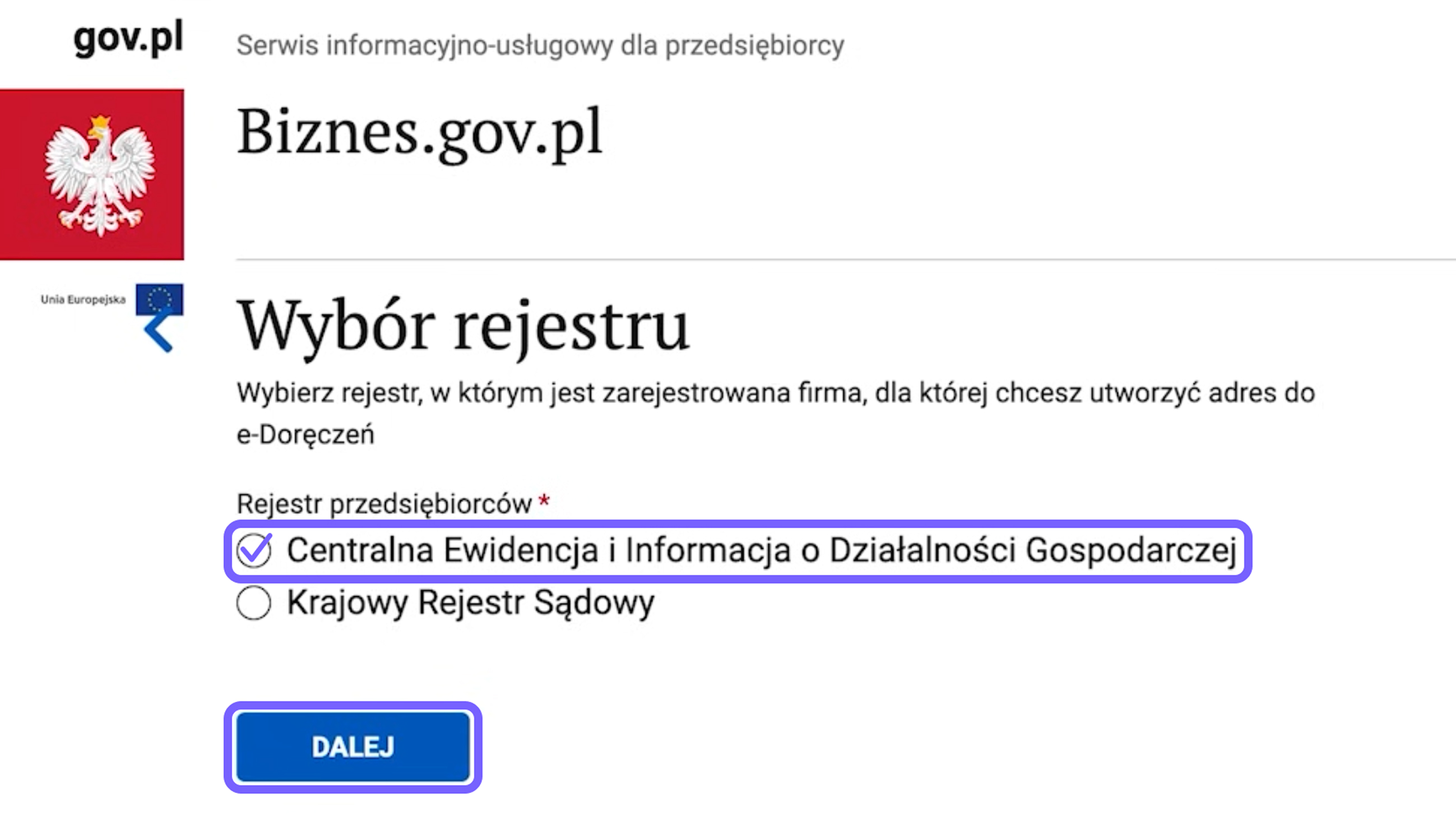

Step 3. Select the business register

On the next screen, select:

Centralna Ewidencja i Informacja o Działalności Gospodarczej — Central Register and Information on Economic Activity, CEIDG.

This option is intended for sole traders operating as a jednoosobowa działalność gospodarcza, or JDG.

Click Dalej — Next.

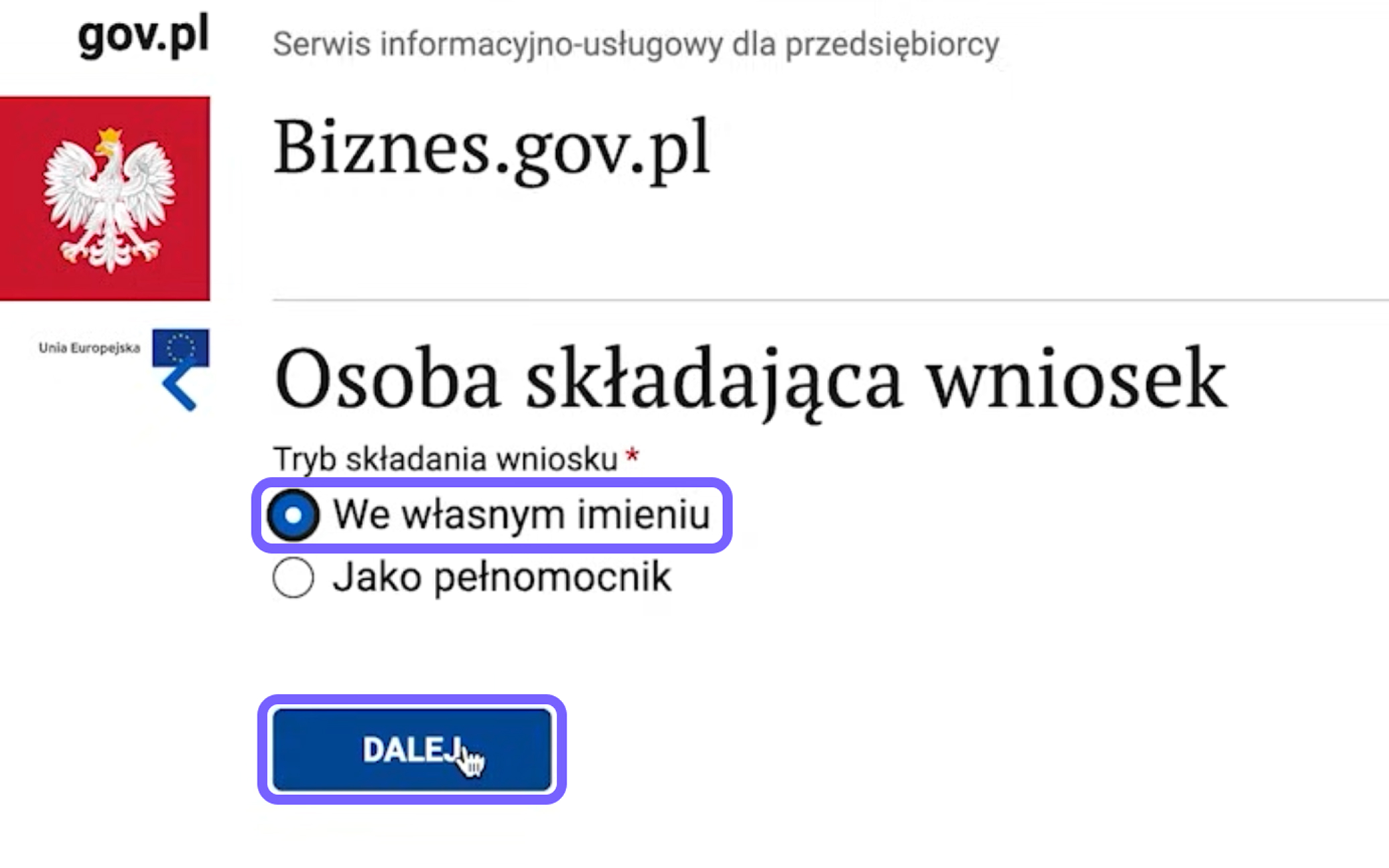

Step 4. Specify on whose behalf the application is being submitted

When creating an address for your own business activity, select:

We własnym imieniu — On my own behalf.

Then click Dalej — Next.

If the application is being submitted by an authorised representative, the process and required documents may be different.

Step 5. Check and complete your details

Some information will be retrieved automatically from CEIDG. Check that the entrepreneur’s details are correct and complete any missing fields.

In particular, verify:

first name and surname;

PESEL number;

NIP and REGON numbers;

registered business name;

contact details;

regular email address.

Technical notifications will be sent to the email address provided, including information about the application status and instructions for activating the inbox.

A regular email address does not replace e-Doręczenia. It is used only for notifications.

After checking the information, click Dalej — Next.

Step 6. Decide whether a separate administrator is needed

The system will ask whether you want to appoint an inbox administrator.

If the entrepreneur intends to manage the inbox personally, they may select the option without appointing a separate administrator.

If another person will manage access and settings, their details must be provided. The administrator may, among other things:

manage users;

grant and withdraw access;

configure permissions;

work with correspondence within the scope of their permissions.

A separate administrator is not mandatory for a standard JDG. An accountant can be added as a user after the inbox has been activated.

Click Dalej — Next.

Step 7. Accept the terms and conditions

Read the terms governing the service and confirm your acceptance.

Select the relevant box next to Regulamin — Terms and Conditions, then click Dalej — Next.

Step 8. Confirm the declarations

The next screen will display the required declarations — oświadczenia.

Read them and select the necessary boxes to confirm that the information provided is correct.

Then click Dalej — Next.

Step 9. Check the public authority

The system will automatically display the authority responsible for processing the application.

Check the information and click Dalej — Next. In most cases, you do not need to search for or select the authority manually.

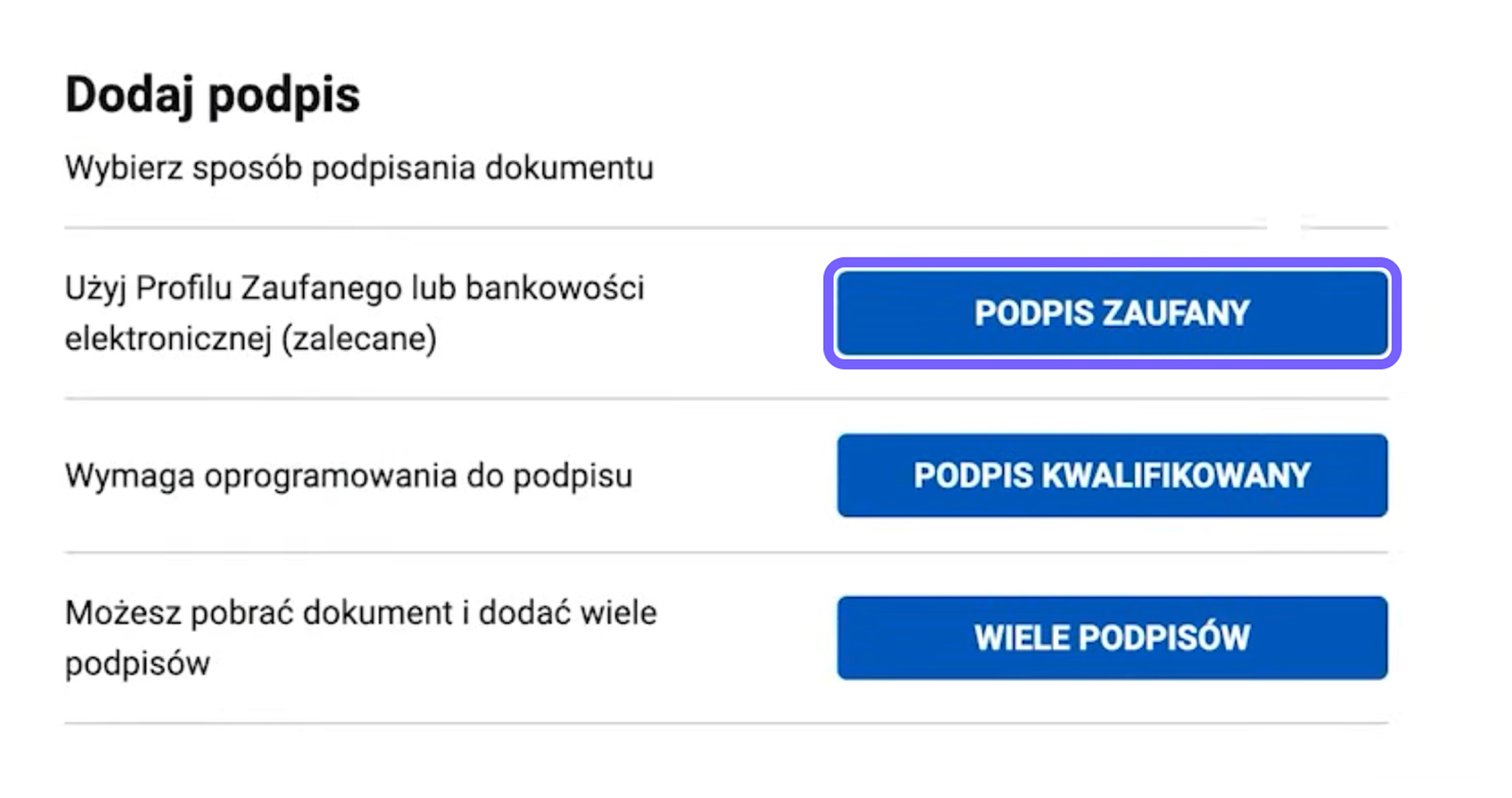

Step 10. Sign the application

After reviewing the application, select your electronic signature method.

When using Profil Zaufany, click:

Podpis zaufany — Trusted signature

and then:

Podpisz podpisem zaufanym — Sign with a trusted signature.

The system will redirect you to the identity confirmation page. Log in and confirm the signature.

After returning to the application, make sure that the signature has been added.

Step 11. Submit the application

After signing, click Wyślij — Send.

A submission confirmation will appear on the screen. The document will also be available in the entrepreneur’s account.

It is advisable to save the confirmation or application reference number until the registration process has been completed.

Step 12. Wait for the instruction email

Once the application has been processed, an email confirming the creation of the e-Doręczenia address will be sent to the address provided earlier.

The email will explain what must be done to activate the inbox.

Important: submitting the application does not mean that the inbox is already active. You must follow the instructions in the email and complete the activation process.

Step 13. Activate the inbox

Follow the instructions in the email or log in again to Konto Przedsiębiorcy on Biznes.gov.pl.

Then:

open the e-Doręczenia section;

select the newly created address;

proceed to activation;

check the notification email address;

accept the operator’s terms and conditions if required;

click Aktywuj skrzynkę — Activate the inbox.

After activation, the address will be entered into the Electronic Address Database, BAE. From that point, public authorities will be able to send official correspondence to it.

What to do after activation

After logging in for the first time, it is advisable to:

check the notification email address;

confirm that the inbox status is active;

arrange regular monitoring of incoming messages;

give the accountant access if they will handle correspondence;

appoint an additional administrator if necessary;

establish a procedure for storing messages and delivery confirmations.

Do not rely only on notifications sent to a regular email account. The responsible person should also log in to the e-Doręczenia inbox regularly.

How to give an accountant access

A business owner or sole trader does not have to process every incoming message personally. Access can be granted to an accountant, lawyer, or another responsible employee.

Only the inbox administrator can add users and manage their permissions.

The system includes several standard roles:

Właściciel — Owner: the inbox owner;

Administrator: manages users, roles, and settings;

Uprawniony — Authorised user: can work with correspondence within the permissions granted;

Obserwator — Observer: has limited access, for example read-only access.

The administrator can also create additional roles with a selected set of permissions.

To add an accountant, the administrator should:

log in to the business inbox;

open the user management section;

select the option to add a new user;

enter the user’s details and email address;

assign the appropriate role;

send the invitation.

The invitation is valid for 14 days. Once it has been accepted, the user’s status changes to active, and they receive access to the inbox according to the assigned role.

Access is always granted to a specific individual. If an employee leaves the company or cooperation with an accounting firm ends, their permissions must be withdrawn.

Businesses may also appoint several administrators to reduce operational risk. This helps preserve access to inbox management if the main administrator is absent or no longer works with the organisation.

How to organise e-Doręczenia within a business

After activating the inbox, it is advisable to establish an internal procedure for handling official correspondence.

A basic procedure may include:

checking incoming messages every working day;

notifying the manager or client about a new document;

recording the date of receipt and response deadline;

appointing the person responsible for preparing the reply;

saving proof of sending and receipt;

regularly archiving correspondence;

reviewing the list of users and their permissions.

The inbox provided by the public service provider has a guaranteed capacity of 3 GB for non-public entities. A received message remains available in the system for 180 days from the date of delivery.

Messages, attachments, and proof of sending and receipt should therefore be saved regularly in the company’s internal archive.

For a standard message sent to no more than 15 recipients, the maximum total size, including attachments, is 500 MB.

How much does e-Doręczenia cost?

Creating an address and using the public inbox to communicate with public authorities is free of charge for the entrepreneur.

Sending documents from a company or individual to a public authority through the public PURDE service costs PLN 0. The public authority covers the cost of correspondence it sends.

Legally valid correspondence between companies uses paid e-Doręczenia services. It may be provided by a qualified service provider or as an additional service offered by the selected operator.

Availability and pricing depend on the provider’s terms.

Frequently asked questions

Are notifications sent to a regular email address?

Yes. An email address can be added in the settings to receive notifications about new messages.

However, a regular email account is used only for notifications. The official document must be opened in the e-Doręczenia inbox.

Can a personal inbox be used for sole trader activity?

No. A separate business address must be created for activity registered in CEIDG.

Should messages be saved separately?

Yes. Inbox storage is limited, and some documents may be needed several years later.

It is advisable to save the message together with proof of sending and receipt.

Can the entire inbox be managed by an accountant?

An accountant can be granted access and the necessary permissions. However, the business owner remains responsible for controlling who has access and how deadlines are monitored within the business.

What should be done now?

Entrepreneurs registered in CEIDG before the end of 2024 do not have to wait until September 2026. The inbox can be created earlier, giving the business time to test the system and establish a clear procedure for handling correspondence.

Before implementation, check:

whether the entrepreneur or company has an active address in BAE;

who has been appointed as administrator;

whether the notification email address is current;

whether the accountant has the required access;

whether correspondence is archived regularly;

who is responsible for monitoring response deadlines.

Need help organising e-Doręczenia?

The ELP Office team will help you understand the necessary steps, arrange access for the responsible accountant, and establish a clear process for handling official correspondence.

This material is provided for informational purposes only. Individual legal and tax matters should be discussed with a qualified specialist.

While salaried employees are automatically insured against all risks, for a sole proprietor (JDG), sickness insurance (dobrowolne ubezpieczenie chorobowe) is strictly voluntary. The entrepreneur must independently submit an application to ZUS to be included in this insurance system. It is these contributions that give you the right to receive maternity and paternity benefits.

Key leave rules for sole proprietors (applicable to all types of leave):

No waiting period (0 days): Unlike regular sick leave, which requires paying contributions for 90 days, the right to maternity benefits arises literally from the first day of paying the chorobowe contribution. If you manage to activate the insurance before giving birth, you are entitled to the benefit.

You can continue running your business: The legislation does not restrict your freedom of action. You can legally manage the company, issue invoices (faktury), and generate revenue right while receiving the benefit.

Alternative: official suspension (Zawieszenie): If you do not plan to issue invoices and work in the first months after childbirth, the business can be officially suspended. A crucial legal nuance: if the company was active and contributions were paid at the time of birth, subsequent suspension of activities will not interrupt the cash flow from ZUS. The right to the benefit is already secured for you, and the suspension will reduce the administrative burden and even the payment of health insurance to zero.

Micro-debts are allowed: On the day the insured event occurs (childbirth), your total debt to ZUS must not exceed 1% of the minimum wage (in 2026, this limit is 48.06 PLN). If the debt is less than this amount, payments will begin as usual. If the debt exceeds the limit, the right to payment is suspended, but you will have exactly 6 months to pay it off in full, after which ZUS will pay the benefit retroactively.

The Universal Minimum Rule (Kosiniakowe)

Even if you paid minimum contributions, the state will back you up. The Kosiniakowe rule applies: if, after all calculations, the benefit of the insured entrepreneur is below 1,000 PLN net per month, ZUS automatically guarantees a top-up to this amount.

Example: If you paid contributions from the preferential base (Preferencyjny ZUS) for a short time, the calculated benefit amount may be low (e.g., 350 PLN net). In this case, ZUS automatically compensates the difference (650 PLN) from the state budget. This state top-up is completely exempt from income tax (PIT).

Important clarification: This rule applies only to maternity and parental leave and does not apply to paternity leave (urlop ojcowski). You also need to consider taxes: ZUS first calculates the base amount, deducts the tax advance (PIT), and only if the net amount is less than 1,000 PLN does it compensate the difference.

Timeline: 3 Types of Leave for Parents

To maximize financial benefits and time with the child, parents can flexibly combine three types of leave. The state system works as a single mechanism: even if one parent is employed (Umowa o pracę) and the other runs a JDG, you can still share the total quotas between yourselves.

Maternity Leave (Urlop macierzyński): The primary, basic leave for the mother. It lasts 20 weeks (for the birth of one child) and is granted immediately after the baby is born.

Parental Leave (Urlop rodzicielski): A shared pool of time (up to 41 weeks) that can be flexibly divided between parents. The exception is the 9 "non-transferable" weeks, which are strictly reserved for the second parent (most often the father).

Paternity Leave (Urlop ojcowski): A short 14-day leave exclusively for the father. It is paid at a 100% rate and expires when the child turns 1 year old.

Let's take a closer look at each one.

Maternity Leave (Urlop macierzyński)

Maternity leave is the first and mandatory stage of support. Its basic duration depends on the number of children born:

1 child: 20 weeks (140 days).

2 children (twins): 31 weeks (217 days).

Number of children at one birth

Leave duration

Equivalent in days

1 child

20 weeks

140 days

2 children (twins)

31 weeks

217 days

3 children (triplets)

33 weeks

231 days

4 children

35 weeks

245 days

5 or more children

37 weeks

259 days

Recommendation: Although the law allows you to start maternity leave 6 weeks before childbirth, financially, this is not the most advantageous decision. It is much more effective to take regular pregnancy sick leave (Zwolnienie lekarskie — code B) prior to the birth. It is paid at a rate of 100% of the base, and all your legal 20 weeks of maternity leave will be preserved for use after the baby is born!

How Benefits Are Calculated: Two Strategies

Payouts are calculated based on your ZUS base for the last 12 months. You have two paths, and the choice depends on how quickly you submit your application to ZUS. To understand the real numbers, it is important to know the current ZUS bases for 2026:

Type of insurance regime (2026)

Base calculation algorithm

Statutory base (PLN)

Preferencyjny ZUS (Preferential)

30% of the minimum wage (4,806 PLN)

1,441.80

Duży ZUS (Full/Standard)

60% of the projected average wage (9,420 PLN)

5,652.00

It is from these amounts that the payout percentages will be calculated depending on the strategy you choose:

Stability Strategy (81.5% rate): If you submit one general application for both leaves (maternity + parental) within 21 days after childbirth, ZUS will pay you 81.5% of your calculated base throughout the year. This is the most popular option, ensuring a steady cash flow.

Stepped Strategy (100% / 70% rate): If you miss the 21-day deadline or submit applications separately (first for maternity, and half a year later for parental), the first 20 weeks will be paid at a 100% rate, and the subsequent parental leave at a 70% rate.

Parental Leave (Urlop rodzicielski) and the Father's Quota

The right to take parental leave (urlop rodzicielski) arises immediately after the end of maternity leave (or from the moment of the child's birth if the mother does not have insurance). This is a logical continuation of support, but with one fundamental difference: this leave is intended for both parents.

The basic total duration of this leave for the birth of one child in 2026 is 41 weeks (for twins — 43 weeks). According to Work-Life Balance rules, neither parent can claim this entire duration for themselves.

Leave Architecture:

Maximum for one parent: 32 weeks (this is the absolute maximum a mother or father can take individually).

Non-transferable quota: 9 weeks. Exclusively reserved for the second parent (most often the father). These weeks cannot be transferred to the mother — if the father declines the leave, they are simply canceled.

The remaining weeks can be divided between the parents in any proportion or used simultaneously.

Key Conditions of Parental Leave

The mechanics of this leave give entrepreneurs maximum flexibility in planning their time and finances. The following accommodating conditions apply to JDG payers:

Freedom of timing: The leave does not necessarily have to be taken immediately after maternity leave ends. You can use it at any time up until the end of the calendar year in which the child turns 6.

Can be split: You are not obligated to take all the weeks in one block. The leave can be divided into a maximum of 5 parts.

Simultaneous use: Mom and dad can be on parental leave at the same time. For example, you can take a portion of the shared quota and spend a month at home together.

Legal work: As with maternity leave, while receiving the benefit, you can continue to conduct business operations, manage the company, and issue invoices.

Benefit Amount: The payout amount during parental leave directly depends on the strategy you chose when submitting documents right after childbirth (detailed in the section above).

Special Conditions for an Entrepreneur Father (Dodatkowy rodzicielski)

Returning to the 9 weeks strictly reserved for the father. If the father is also an entrepreneur, the following payout rules apply to him:

Cannot be transferred to the mother: If the father opts not to take the leave, this period is simply nullified.

Separate calculation base: The benefit for this period is calculated based on the father's individual ZUS base and amounts to 70% of this base.

Immediate payouts: There is no need to wait 3 months after setting up voluntary chorobowe insurance; the right is established immediately provided the insurance is active.

Deadlines: These 9 weeks can be used (in a single block or several parts) until the end of the calendar year in which the child turns 6.

And yes, the father can continue running his business and issuing invoices during this leave!

Addition: If the mother is insured with ZUS but for some reason did not use her share of the parental leave, the father can claim the main portion for himself (up to 32 weeks). This requires a written statement (oświadczenie) from the mother. Important: If the spouse does not have insurance and receives state aid for mothers (świadczenie rodzicielskie) through MOPS or Urząd, the entrepreneur father will not be able to claim these shared 32 weeks from ZUS. However, his personal non-transferable quota of 9 weeks remains securely his under any circumstances!

Paternity Leave (Urlop ojcowski)

This is a separate entitlement, independent of the mother's maternity leave. Entrepreneur fathers have the right to 14 calendar days of leave, financed at 100% of the father's individual ZUS base.

Key features:

Strict deadlines: The leave must be utilized strictly before the child reaches 1 year of age (12 months). It can be taken entirely as one block (14 days) or split into two equal halves (7 days each).

Double benefit: You have the legal right to reduce your ZUS social contribution obligations proportionally to the days of your leave. For "Duży ZUS" payers in 2026, the savings for 14 days will amount to approximately 899 PLN.

Business doesn't stop: You can continue to sign contracts and issue invoices directly during this leave.

Taxation (PIT) and exemptions: By default, the paternity leave benefit is subject to standard tax (12% advance), just like other ZUS disbursements. However, you have the opportunity to achieve absolute PIT-0 if you qualify for one of 4 targeted reliefs: you are under 26 (Ulga dla młodych), you have 4 or more children, you qualify for the return relief (repatriation), or you are a working pensioner. In these scenarios, the payout is tax-exempt.

Instructions: Paperwork and ZUS Contribution Optimization

Here we have consolidated all the bureaucratic steps required to properly formalize your payouts.

When transitioning into any of the listed leaves, the state assumes the payment of your social contributions (pension and disability). However, ZUS does not update this data automatically! You must independently update your status within 7 days from the start date of the specific leave. During the benefit period, the entrepreneur is only obligated to pay health insurance (ubezpieczenie zdrowotne).

What to do in ZUS (via the PUE/eZUS platform):

Temporarily deregister from full social insurances (form ZUS ZWUA).

Register exclusively for zdrowotne by changing the registration code (form ZUS ZZA).

Legal contribution optimization: Typically, when switching to zdrowotne via the ZZA form, the standard code 05 10 00 is used. But if your benefit is small and the state tops it up to 1,000 PLN under the Kosiniakowe rule, use the special code 05 80 00 (or 05 81 00). This grants you the legal right to skip paying even the health insurance.

What documents to submit for the benefit:

Regardless of who is taking the leave or what kind of leave it is, you will always need:

ZUS Z-3b (a special income certificate for entrepreneurs (JDG), which serves as the basis for calculating the benefit amount).

Akt urodzenia dziecka (a copy of the child's birth certificate).

Additionally, append the following depending on the specific leave you are applying for:

Maternity + Parental (Single application):ZUS ZAM — The unified universal form for maternity benefit applications. This form is used if the mother wishes to declare her intent to take both maternity and parental leave as a single continuous block within 21 days of birth (to lock in the 81.5% rate).

Maternity Leave only:ZUS ZAM — standard application for urlop macierzyński.

Parental Leave (for mom or dad):ZUS ZUR — application for urlop rodzicielski. Additionally: if one parent claims the shared portion of the leave (e.g., the father takes 32 weeks instead of the mother), you must attach an Oświadczenie drugiego rodzica (a declaration from the second parent confirming they are not utilizing their share).

Paternity Leave (14 days):ZUS ZAO — the exclusive application for dads for urlop ojcowski.

Returning to Work

After the leave concludes, the procedure must be repeated in reverse: you need to deregister from zdrowotne (ZWUA) once again and submit form ZUS ZUA to restore your full insurance package. During this process, you have the legal right to proportionally reduce your social contributions for the month in which you were on leave (for instance, for those 14 days of paternity leave).

When you commence maternity leave, your voluntary sickness insurance is canceled automatically. Therefore, when submitting the ZUA form upon returning to work, you are strictly obliged to check the box again to confirm your desire to rejoin the voluntary sickness insurance scheme (dobrowolne ubezpieczenie chorobowe) within 7 days. If you neglect to check this box, your continuity of insurance will be broken, and you will forfeit the right to paid sick leave (L4) in the future.

Contribution Holidays (Wakacje składkowe)

When mapping out maternity leaves, do not overlook the current support mechanism available for micro-entrepreneurs. Once per calendar year, you have the right to select one month of complete exemption from paying social contributions. In 2026, for Duży ZUS payers, this translates to savings of 1,926.76 PLN for the month.

You cannot utilize these contribution holidays during the same month you receive maternity benefits. However, it serves as an ideal strategic asset that can be activated immediately before heading into maternity leave or directly after returning to work. Furthermore, an entrepreneur father can take his 14 days of paternity leave in one month and the contribution holidays in a subsequent month, thereby maximizing the overall financial support extracted from the state.

Disclaimer: This article is for informational purposes only and relies on current ZUS data for 2026. Every entrepreneur's situation is unique, and legal interpretations may evolve. For precise benefit calculations and tailored tax strategy planning, we strongly recommend booking an individual consultation with an accountant.